Are You Selling Your Company? Be Careful with Financial Buyers!

by Scott Edward Walker on February 9th, 2020Introduction

I’ve been doing M&A transactions for 25+ years (including nearly eight years at two major New York City law firms), and I’m going to discuss an important issue for founders interested in selling their company: the distinction between strategic and financial buyers. Most founders are familiar with strategic buyers, such as Google, Facebook and other big companies; they are not, however, familiar with financial buyers. This post briefly discusses the differences between such buyers and expressly warns founders to watch-out for financial buyers.

What Are Financial Buyers?

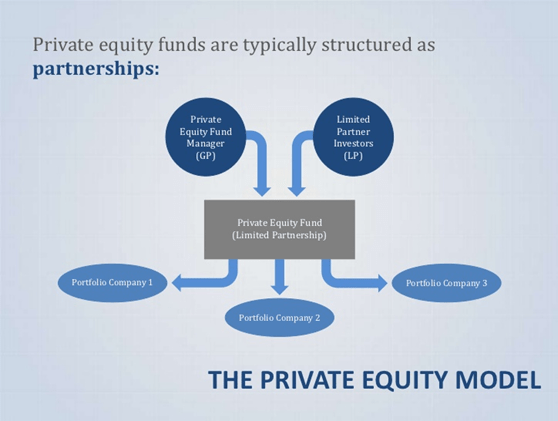

Financial buyers are investors that are interested in a return on their investment business – which is the business of buying and selling companies. Instead of investing in the stock market or in startups (i.e., venture capital), they buy and sell companies and seek a return that way. The most common financial buyer is a private equity firm. Indeed, big private equity firms (such as Blackstone, TPG, Apollo, etc.) are often on the front pages of the Wall Street Journal. There are also, however, lots of small private equity firms that you never read about and which are on the hunt for small, private companies. (Hedge funds and family offices are also financial buyers.)

Why Are Financial Buyers Different Than Strategic Buyers?

Financial buyers are different from strategic buyers because, as noted above, they are merely looking for a return on their investment. Moreover, because most financial buyers are set-up as funds (which have their own limited partner investors) that typically expire in 10 years, the return on their investment must happen relatively quickly. In other words, the business model for financial buyers is to buy a business and then sell it (or take it public) within a relatively short period of time. Every aspect of the M&A transaction flows from this. Simply put, unlike strategic buyers, financial buyers are not typically purchasing your company for the long term or as a result of potential synergies.

Why Does the Type of Buyer Matter?

It matters because, unless you understand the motivation of a prospective buyer, it will be very difficult to make informed decisions with respect to critical deal issues. For example, as discussed below, the deal structure with financial buyers is usually different than with strategic buyers; and, most importantly, financial buyers typically offer a lower purchase price (and less cash at closing). Moreover, you will typically be dealing with very different types of individuals. The principals at private equity firms are extremely sophisticated and savvy, and have often developed an extraordinary skill set in connection with buying and selling companies and wooing founders. Again, this is what they do for a living. Unless you are dealing with a large strategic buyer with a corporate development division, you will typically be negotiating with the CEO and/or CFO of a strategic buyer, who is just looking to get the deal done and not trying to nickel and dime you and extract every possible financial advantage (i.e., is not merely seeking a return on investment).

How Is the Deal Structure Different with a Financial Buyer?

If you have never done a deal with a financial buyer, you are in for a rude awakening. The deals are typically extremely complex because the name of the game is debt. Financial buyers buy companies the same way most individuals buy homes: they pay a cash down payment and borrow the balance. In order to juice their returns, financial buyers try to borrow as much as possible in connection with a particular deal, which usually means that 70-80% of the purchase price will be debt. Now don’t misunderstand this — the financial buyer is not typically borrowing from the seller; they are borrowing from banks and subordinated lenders. The issue for you is that the acquisition agreement may contain a financing condition, which means that if they do not get their financing they may walk away with no recourse. This is one of the unusual structures with a financial buyer. Another unusual structure is that financial buyers will typically require you, as the founder/CEO, to rollover your equity (usually 20-30%) into a new acquiring entity. This means that you will only get 70-80% at closing, and probably closer to 50-60% – because they will push hard for a huge escrow and often an earnout. The bottom line is that debt creates complexity, which creates extraordinary documentation — which creates time, money and uncertainty for the founder.

Should I Avoid Financial Buyers?

Like with any transaction, you need to diligence the party on the other side of the table. Simply put, you need to do your homework and talk to other parties that have dealt with them in order to make an informed judgment as to whether they are guys with whom you should be negotiating. Obviously, sometimes you have no choice but to deal with the financial buyer. But, ideally, you want to create a competitive environment where you’re playing different prospective buyers off of each other in order to negotiate the best possible deal terms. As I have previously discussed, this all should happen in connection with the negotiation of a term sheet or letter of intent, which is when you, as the seller, have the most leverage. The best advice I can give founders in connection with any sale is that cash at closing is king. Anything other than cash at closing creates uncertainty and possible litigation – whether it is money held in escrow, rollover equity in a new LLC, an earnout, a promissory note, etc. In short, strategic buyers typically provide the most cash at closing.

Conclusion

The foregoing is a brief overview of the differences between financial buyers and strategic buyers. When I worked at two major law firms in New York City, I represented a number of private equity firms and hedge funds in connection with buying and selling companies. Indeed, I saw all the games they play at a personal level and in connection with financial engineering. Now I am on the other side of the table, and I have recently helped founders successfully negotiate with my old clients.